The MAGA Child Savings Account: What Every Parent Needs to Know

If you’re a current or soon-to-be parent, there’s a new financial tool you should be aware of: the MAGA Account (Money Account for Growth and Advancement). Introduced as part of current President Donald Trump’s “One Big Beautiful Bill,” this program aims to jump-start financial savings for the next generation.

Here’s a full breakdown of what MAGA Accounts are, how they work, and what it means for your family.

What is a MAGA Account?

The MAGA Account is a federally backed savings program designed to help children build long-term financial security. Referred to as “Trump Accounts,” these are government-seeded investment accounts for eligible newborns and young children.

Key Features

- Initial $1,000 Government Contribution: Each eligible child receives $1,000 deposited by the federal government.

- Annual Contribution Limit: Up to $5,000 per year in after-tax contributions can be made by parents, guardians, relatives, or even employers.

- Investment Strategy: Funds are invested in a U.S. equity index fund managed by private financial firms with Treasury oversight.

- Access Timeline:

- 50% of the funds can be withdrawn at age 18.

- Full access at age 25.

- All funds must be withdrawn by age 30.

- Qualified Uses: Education, first-time home purchase, or starting a business (subject to favorable tax treatment).

Who is Eligible?

- Children born between January 1, 2025, and December 31, 2028.

- Some children under 8 years old born before 2025 may also qualify, depending on final implementation rules.

Common Questions & Answers

Q: Can I open a MAGA account for my child myself? A: MAGA accounts will be automatically opened for eligible children. Parents or legal guardians can then manage the account and contribute to it.

Q: What happens if the account is not used by age 30? A: Funds must be withdrawn by age 30. If not, unused money may revert to the government or be penalized depending on regulations.

Q: Are earnings tax-free? A: Earnings grow tax-deferred. Withdrawals for qualified uses are taxed at the long-term capital gains rate. Non-qualified uses may incur a 10% penalty and regular income tax.

Q: How does this affect college financial aid? A: Since the account is in the child’s name, it may be counted as a student asset, which can reduce eligibility for need-based financial aid.

Q: How is this different from a 529 plan? A: Unlike 529 plans, MAGA accounts can be used for more than just education, but they don’t offer tax-free withdrawals. They are also not state-managed.

Pros and Cons for Parents to Consider

Pros:

- Free $1,000 start for your child.

- Encourages early investment and financial literacy.

- Flexibility in how funds are used.

Cons:

- Earnings are taxed upon withdrawal.

- Potential to reduce financial aid.

- Political branding may influence future changes to the program.

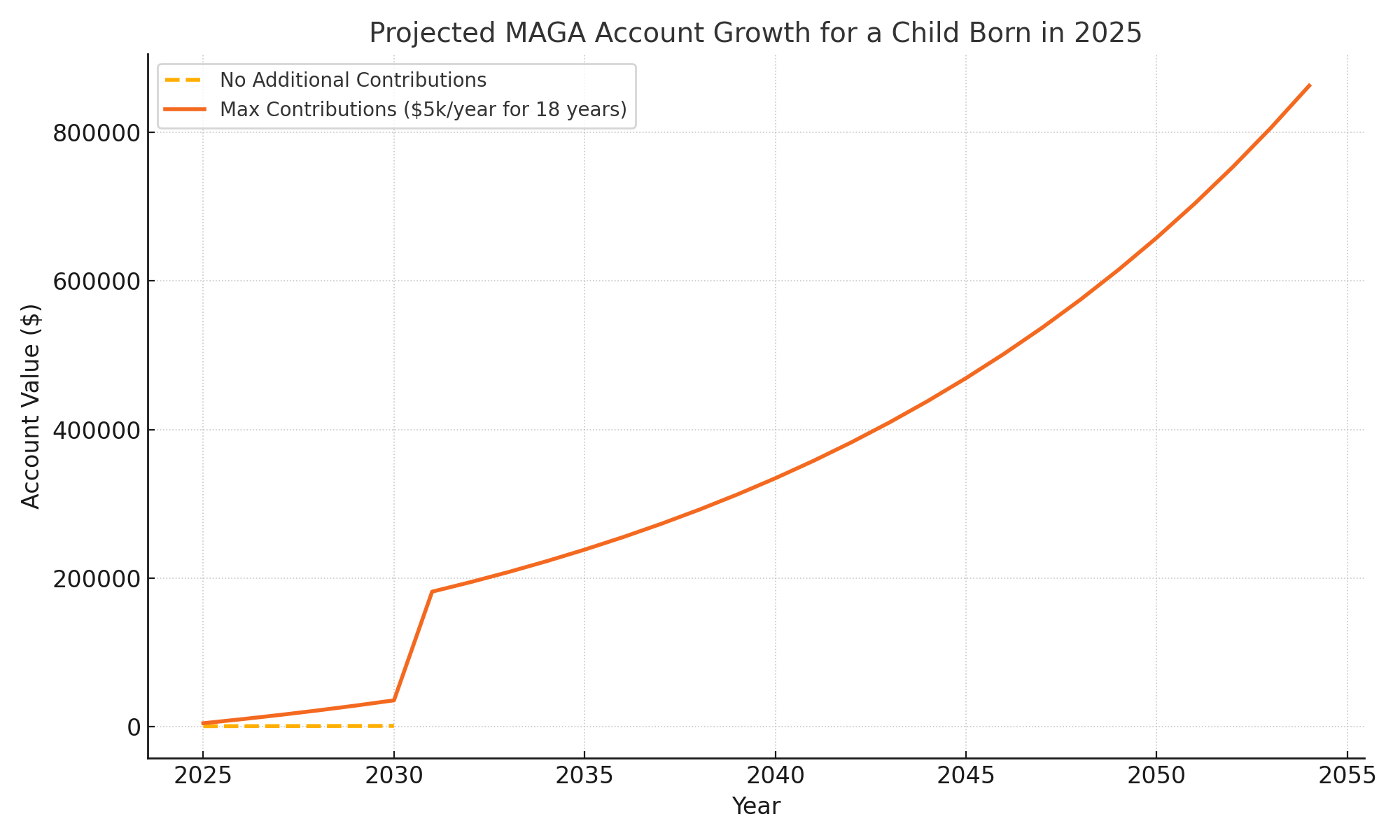

How Much Could Your Child Have?

Let’s explore two financial projections for a child born in January 2025, assuming an average annual return of 7% from a U.S. equity index fund:

Scenario 1: No Additional Contributions

- By Age 18:

The initial $1,000 government deposit would grow to approximately $3,400. - By Age 30:

That same $1,000 left untouched could grow to around $7,600.

Scenario 2: Maxed Out Contributions ($5,000/year)

- Over 18 years, parents could contribute up to $90,000 total.

- By Age 18:

The account could be worth approximately $170,000, assuming consistent contributions and market performance. - By Age 30 (no additional contributions after 18, just compounding):

The account could grow to around $336,000.

Note: These figures are estimates. Actual results depend on market performance, investment fees, and contribution timing.

How to Track and Manage a MAGA Account

- Access and Management: MAGA accounts will likely be accessible via a secure government portal or financial partner platform. Expect features like an online dashboard and potentially a mobile app to monitor contributions, growth, and usage.

- Family Contributions: Contributions can come from parents, grandparents, and even employers. These might be done via gifting links or account routing numbers.

- Account Statements: Parents should receive periodic statements—quarterly or annually—detailing account performance and contributions.

Tax Planning Tips for MAGA Accounts

- Tax Treatment: Growth is tax-deferred. Qualified withdrawals (education, home, business) are taxed at favorable long-term capital gains rates. Non-qualified withdrawals incur income tax and a 10% penalty.

- Gifting Strategy: Contributors can use the IRS annual gift tax exclusion (currently $18,000 per person in 2024) to avoid triggering gift taxes.

- Compared to Other Accounts: MAGA accounts offer broader use than 529 plans but less favorable tax treatment. They don’t require earned income like a Roth IRA for kids.

Strategic Uses for MAGA Funds

- For College: Use alongside a 529 to cover expenses that fall outside tuition and textbooks (e.g., housing, travel, business projects).

- For Homeownership: Apply MAGA funds to a first-time home down payment in early adulthood.

- For Entrepreneurship: Start a small business or side hustle—especially valuable for teens and young adults not pursuing traditional college paths.

Talking to Your Child About Their MAGA Account

- Ages 5–10: Introduce the idea of “your special growing savings account.”

- Ages 11–15: Explain investing and compound growth in simple terms.

- Ages 16–18: Include them in financial planning, review statements, and discuss future plans for the money.

What to Watch Out For

- Political Shifts: Since this is a Trump-branded initiative, future administrations could modify or terminate the program.

- Impact on College Aid: Because the account is in the child’s name, it could reduce eligibility for need-based college aid.

- Single-Bucket Risk: Avoid relying solely on one savings tool. Diversify with 529s, Roth IRAs (if the child has income), and traditional savings.

MAGA Account Quick Facts – At a Glance

| Feature | Details |

|---|---|

| Initial Government Contribution | $1,000 |

| Annual Contribution Limit | $5,000 (after-tax) |

| Access Timeline | 50% at age 18, full at 25, must be used by 30 |

| Qualified Uses | Education, home purchase, or business startup |

| Tax Treatment | Tax-deferred growth; LTCG on qualified use |

| Financial Aid Impact | Considered a student-owned asset |

| Longevity Risk | May be affected by future political changes |

Final Thoughts

Whether you’re expecting a child soon or raising young ones already, the MAGA Account program could offer a unique opportunity to set up long-term financial security. While it’s not without limitations, the government-seeded contribution and flexibility make it worth considering alongside more traditional savings options like 529 plans.

As with any financial decision, consult with a financial advisor to see how this fits into your broader savings goals.

Stay informed, plan smart, and give your child a head start!